Every year, over thirty percent of American homeowners experience storm damage that leaves their roofs vulnerable and their property investments at risk. In Corpus Christi and San Antonio, fast-changing weather can expose unexpected myths about roofing claims, leading to costly mistakes with insurance companies. This guide cuts through confusion, highlighting what truly matters for residents seeking prompt, expert support to protect their homes and secure fair insurance outcomes after severe storm events.

Table of Contents

- Defining Roofing Claims And Common Myths

- Types Of Roof Damage Covered By Insurance

- Replacement Cost Vs. Actual Cash Value Policies

- Filing Timeframes And Documentation Requirements

- Financial Implications And Deductibles Explained

- Common Pitfalls And How To Avoid Them

Key Takeaways

| Point | Details |

|---|---|

| Understanding Roofing Claims | Homeowners must recognize that not all roof damage qualifies for insurance claims and that specific documentation is essential for successful recovery. |

| Policy Coverage Awareness | Homeowners should familiarize themselves with the types of roof damage covered by their insurance to ensure they have appropriate financial protection. |

| Choosing the Right Policy | Selecting between Replacement Cost Value and Actual Cash Value policies requires careful consideration of the home’s condition and potential out-of-pocket risks. |

| Timeliness and Documentation | Submitting claims within deadlines and maintaining thorough documentation are crucial steps for maximizing potential insurance recovery. |

Defining Roofing Claims and Common Myths

A roofing claim represents a formal insurance request seeking financial compensation for roof damage, typically triggered by severe weather events like hailstorms, high winds, or hurricane impacts across Texas. These claims are critical pathways for homeowners to restore their property’s structural integrity and protect their most significant investment. Roofing claims involve specific insurance requests that require careful documentation and strategic navigation.

Understanding roofing claims requires debunking several persistent myths that often mislead homeowners. Contrary to popular belief, not all roof damage qualifies for an insurance claim, and contractors cannot guarantee automatic claim approval. Some contractors exploit homeowners by making unrealistic promises or demanding full upfront payments. Construction claims serve as formal dispute resolution mechanisms that provide structured approaches to addressing repair and compensation needs.

Typical roofing claim myths include assumptions that minor damage doesn’t matter, all storm impacts are automatically covered, and insurance companies will always approve repair requests. In reality, homeowners must provide detailed evidence, work closely with insurance adjusters, and understand their specific policy limitations. Successful claims depend on prompt reporting, comprehensive documentation, and working with reputable professionals who understand local insurance regulations and storm damage assessment protocols.

Pro tip: Keep a comprehensive photo and video record of your roof’s condition before and after storm events to strengthen your insurance claim documentation and increase your chances of successful recovery.

Types of Roof Damage Covered by Insurance

Homeowners insurance policies provide comprehensive protection against various types of roof damage, with coverage specifically designed to address unexpected structural challenges. Homeowners insurance typically covers multiple disaster scenarios including windstorms, hail impacts, fire, lightning strikes, vandalism, and damage from falling objects. Understanding the nuanced details of these coverage options is crucial for Texas homeowners seeking financial protection for their roofing investments.

Storm-related roof damage represents a significant concern for Texas property owners, with specific insurance considerations for different damage types. Hail damage can create subtle but serious roof deterioration that may not be immediately visible from ground level. Typical covered scenarios include shingle bruising, granule loss, cracking, and impacts that compromise roof structural integrity. Insurers often evaluate damage based on the extent of deterioration, material type, and the specific mechanisms of the storm event.

Coverage limitations are critical to understand, as not all roof damages qualify for insurance claims. Policies frequently exclude certain events like floods and earthquakes, requiring separate specialized insurance riders. High-risk geographical areas might have percentage-based deductibles or more restrictive coverage terms. Homeowners should carefully review their specific policy language, paying close attention to exclusions, claim filing procedures, and documentation requirements that validate potential roof repair or replacement claims.

This table summarizes key roof damage types covered and not covered by standard insurance policies:

| Damage Type | Typically Covered | Usually Excluded | Special Notes |

|---|---|---|---|

| Wind, Hail, Fire | Yes | Rarely | May need prompt inspection |

| Flood, Earthquake | No | Yes | Requires additional insurance riders |

| Vandalism, Falling Objects | Yes | Rarely | Document thoroughly for claims |

Pro tip: Schedule a professional roof inspection immediately after significant storm events to document potential damage and create a comprehensive visual record for insurance claim purposes.

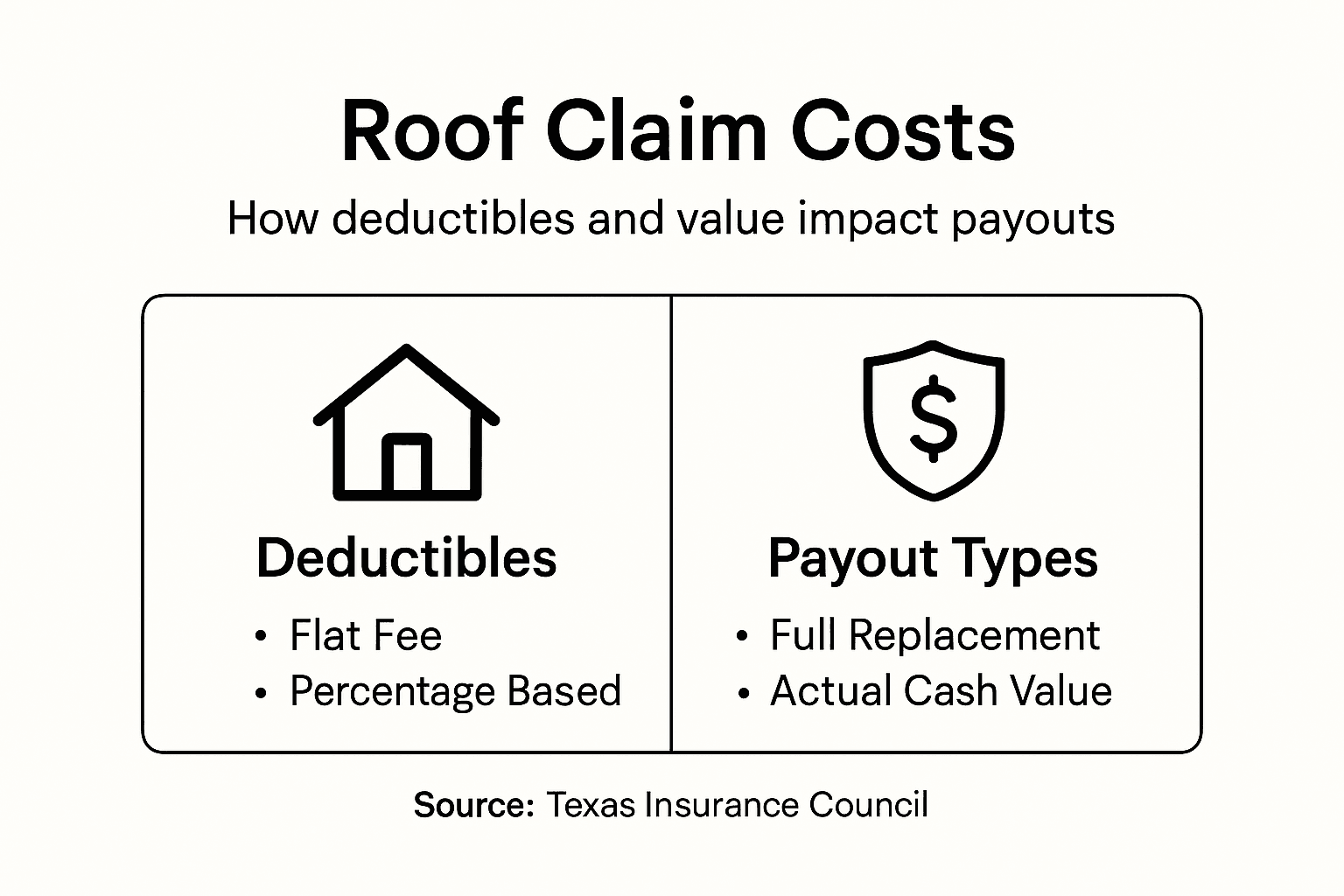

Replacement Cost vs. Actual Cash Value Policies

Replacement Cost Value (RCV) and Actual Cash Value (ACV) represent two fundamentally different approaches to roof insurance coverage that can significantly impact homeowners’ financial outcomes after storm damage. Replacement cost insurance pays full repair expenses without subtracting depreciation, providing comprehensive protection that ensures homeowners can restore their roof to its original condition without substantial out-of-pocket expenses.

Under an RCV policy, insurers cover the complete cost of roof replacement using current market prices for materials and labor, minus the policy deductible. Actual Cash Value policies calculate depreciated property value by considering the roof’s age, existing wear and tear, and overall condition at the time of damage. This means ACV policies typically provide lower reimbursement amounts, potentially leaving homeowners responsible for a more significant portion of repair costs.

Choosing between RCV and ACV requires careful consideration of several factors, including the home’s age, roof condition, and potential repair expenses. RCV policies generally offer more comprehensive protection but come with higher premium costs. Homeowners with newer roofs or those living in areas prone to frequent storm damage might find RCV more financially prudent, as it provides more robust coverage. Older homes or roofs nearing the end of their functional lifespan might benefit from a more cost-effective ACV policy, though this comes with increased financial risk during major repair scenarios.

Here’s a quick comparison of common roof insurance policy types and their financial impact:

| Policy Type | Coverage Method | Out-of-Pocket Risk | Best For |

|---|---|---|---|

| Replacement Cost Value | Full current repair cost, less deductible | Lower, full replacement | Newer roofs in storm-prone areas |

| Actual Cash Value | Depreciated repair value, less deductible | Higher, partial repayment | Older roofs, budget-focused owners |

Pro tip: Request a detailed comparison of RCV and ACV policy terms from your insurance provider, focusing on specific coverage limits, depreciation calculations, and potential out-of-pocket expenses for roof repairs.

Filing Timeframes and Documentation Requirements

Roof damage insurance claims require precise timing and meticulous documentation to ensure successful recovery of repair expenses. Insurance companies enforce specific claim filing deadlines that homeowners must carefully navigate, typically requiring submission within one year of the storm event. These strict timeframes demand proactive and organized approaches to documenting roof damage, preserving critical evidence that supports the insurance claim process.

The documentation requirements for roof damage claims are comprehensive and complex. Homeowners must compile a detailed portfolio of evidence, including comprehensive roof inspection reports and repair documentation that validate the extent and origin of the damage. Essential documents include professional roof inspection certificates, detailed photographs showing damage progression, repair estimates from licensed contractors, original roofing sales contracts, maintenance records, and itemized repair invoices. Each piece of documentation serves as critical evidence substantiating the claim’s legitimacy and supporting the requested compensation.

Navigating the insurance claim process requires strategic preparation and thorough understanding of policy-specific requirements. Different insurance providers may have varying documentation standards, making it crucial for homeowners to communicate directly with their insurance representative. Some insurers might require additional specialized documentation, such as weather reports confirming storm dates, expert damage assessments, or historical maintenance records. Incomplete or poorly organized documentation can result in claim delays, reduced settlements, or outright denials, underscoring the importance of a comprehensive and methodical approach to roof damage claims.

Pro tip: Create a dedicated digital folder for storm damage documentation, including timestamped photographs, repair estimates, and correspondence with insurance adjusters to streamline the claims process and maintain a clear evidence trail.

Financial Implications and Deductibles Explained

Homeowners insurance deductibles represent a critical financial consideration in roof damage claims, directly impacting the out-of-pocket expenses and overall claim recovery process. Insurance deductibles are the policyholder’s initial payment before insurance coverage activates, typically structured as either a fixed dollar amount or a percentage of the home’s total insured value. These deductible structures significantly influence the financial strategy homeowners must adopt when preparing for potential roof damage scenarios.

Claim payments factor in complex insurance-to-value calculations that determine final reimbursement amounts. Replacement Cost Value (RCV) policies provide more comprehensive coverage, offering full repair or replacement costs with depreciation considerations. Homeowners can expect part payments upfront, with additional recoverable depreciation released after submitting complete repair documentation. The selected deductible amount directly affects the claim’s financial outcome, with higher deductibles typically corresponding to lower premium costs but increased personal financial risk during actual claim scenarios.

Specialized deductible structures exist for specific weather events, particularly in storm-prone regions like Texas. Named storm deductibles, wind damage deductibles, and hail damage deductibles may have different percentage-based calculations compared to standard homeowners insurance deductibles. These variations can create significant financial variations, potentially requiring homeowners to cover substantially larger out-of-pocket expenses depending on the specific storm event and policy terms. Understanding these nuanced deductible structures becomes crucial for accurate financial planning and risk management in regions frequently experiencing severe weather conditions.

Pro tip: Review your insurance policy’s deductible structure annually and calculate your maximum potential out-of-pocket expenses for roof damage to ensure adequate financial preparedness.

Common Pitfalls and How to Avoid Them

Roof damage insurance claims are fraught with potential mistakes that can significantly compromise homeowners’ ability to recover repair costs. Roof damage inspections require professional expertise to accurately assess and document subtle structural impacts that untrained eyes might overlook. Homeowners frequently make critical errors by attempting DIY damage assessments, failing to document comprehensive evidence, or missing crucial policy filing deadlines that can invalidate otherwise legitimate claims.

Insurance claim navigation involves complex decision-making that extends beyond simple damage reporting. Avoiding common insurance selection mistakes requires strategic understanding of policy details, financial strength of insurers, and comprehensive coverage considerations. Pitfalls include selecting insurers solely based on price, underinsuring property replacement costs, neglecting specialized coverage like flood insurance, and purchasing insufficient liability protection. These oversights can create significant financial vulnerabilities, particularly in storm-prone regions like Texas where roof damage is a recurring risk.

Professional contractors and insurance experts recommend a proactive approach to mitigating claim-related risks. Critical strategies include maintaining detailed photographic documentation of roof conditions before and after storm events, working with certified roof inspectors, understanding precise policy claim windows, and selecting insurance providers with strong track records of fair claims processing. Homeowners should prioritize comprehensive documentation, prompt reporting, and thorough understanding of their specific policy limitations to maximize potential claim recovery and minimize potential disputes.

Pro tip: Create a dedicated digital folder with timestamped photographs, professional inspection reports, and maintenance records to streamline your insurance claim documentation process and enhance claim credibility.

Protect Your Home with Trusted Texas Storm Roofing Experts

Filing roofing claims after Texas storms can be overwhelming. From understanding replacement cost policies to meeting strict documentation requirements the challenges are real. If you want to avoid common pitfalls Buffalo Roofing & Exteriors is here to help. Our expertise in storm damage restoration and professional roof inspections ensures your claim process is supported by clear evidence and expert advice.

Ready to take control of your roof repair needs in Corpus Christi San Antonio or Victoria? Visit our Roofing Archives | Buffalo Roofing & Exteriors for detailed insights and trust our team to deliver reliable service. Don’t wait until minor damage worsens—get your free estimate and learn how we make filing claims straightforward at Buffalo Roofing & Exteriors. Protect your biggest investment today and let us help you rebuild with confidence.

Frequently Asked Questions

What is a roofing claim?

A roofing claim is a formal request to an insurance company for compensation related to roof damage, often from severe weather events like storms or hail.

What types of roof damage are typically covered by insurance?

Homeowners insurance generally covers damage from storms, hail, fire, vandalism, and falling objects, but usually excludes flood and earthquake damage.

How do I document roof damage for an insurance claim?

To document roof damage effectively, take detailed photographs and video evidence of the damage, obtain professional inspection reports, and keep records of any repair estimates and invoices.

What is the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV) policies?

RCV policies cover the full cost of replacing the roof without deducting depreciation, while ACV policies consider the roof’s depreciated value, potentially resulting in lower reimbursement amounts.

Recommended

- What to Do After a Storm Damages Your Roof | Buffalo Roofing & Exteriors | San Antonio to Corpus Christi, TX

- Insurance Claims | Buffalo Roofing & Exteriors | San Antonio to Corpus Christi, TX

- Is Your Siding Ready for Hurricane Season? | Buffalo Roofing & Exteriors | San Antonio to Corpus Christi, TX

- Windstorm Certification | Buffalo Roofing & Exteriors | San Antonio to Corpus Christi, TX

- Don’t Skip Roof Maintenance: Key Risks You Need to Know – white-diamond-pressure

- Roofing Services in Corpus Christi TX