Strong storms can leave Corpus Christi homeowners worrying about their roof’s future and their finances. When wind, hail, and hurricanes hit the Texas coast, understanding your roofing insurance coverage becomes crucial for protecting your home and wallet. This guide breaks down how roofing insurance works, the types of coverage available, and practical tips for making claims so you can recover quickly and avoid costly surprises.

Table of Contents

- Defining Roofing Insurance For Homeowners

- Types Of Roofing Insurance Coverage In Texas

- How Roof Insurance Claims Work

- Windstorm And Weather-Related Coverage Rules

- Common Exclusions And Claim Pitfalls

- Financial Impact And Choosing The Right Policy

Key Takeaways

| Point | Details |

|---|---|

| Understand Coverage Types | Homeowners should evaluate between replacement cost coverage and actual cash value coverage to ensure adequate financial protection for their roofs. |

| Document Roof Condition | Taking detailed photographs and maintaining records of roof condition can facilitate smoother claims processes and protect against disputes with insurers. |

| Review Policy Exclusions | Be aware of common exclusions such as flood damage and gradual wear and tear that may affect claim approvals and financial recovery. |

| Assess Financial Impact | High insurance premiums in Texas necessitate strategic policy selection, balancing coverage quality with affordability to safeguard home investment. |

Defining Roofing Insurance For Homeowners

Roofing insurance represents a critical component of homeowner protection, specifically designed to safeguard your residential roof against unexpected damage. Unlike standard property coverage, roofing insurance focuses specifically on the structural integrity of your home’s most vulnerable external component. Corpus Christi homeowners face unique challenges from severe coastal weather conditions, making comprehensive roof coverage essential.

At its core, roofing insurance provides financial protection for repairs or complete roof replacement when damage occurs from covered events like hurricanes, hailstorms, wind damage, and other extreme weather phenomena prevalent in South Texas. Insurance policies typically offer two primary coverage types: replacement cost coverage and actual cash value coverage. Replacement cost coverage pays the full expense of roof repair or replacement without factoring in depreciation, while actual cash value coverage accounts for the roof’s current age and condition, potentially reducing the total payout.

Homeowners should understand that insurance coverage isn’t universal. Factors like roof age, maintenance history, and the specific cause of damage significantly impact claim approval. Most policies will cover sudden, accidental damage from storms or external events, but gradual deterioration or lack of maintenance might disqualify a claim. Carefully reviewing your policy’s specific terms and understanding the nuanced details of roof damage protection can help prevent unexpected financial burdens.

Pro tip: Before a major storm hits, take comprehensive photos of your roof’s current condition and store them in a secure, cloud-based location to provide clear documentation for potential future insurance claims.

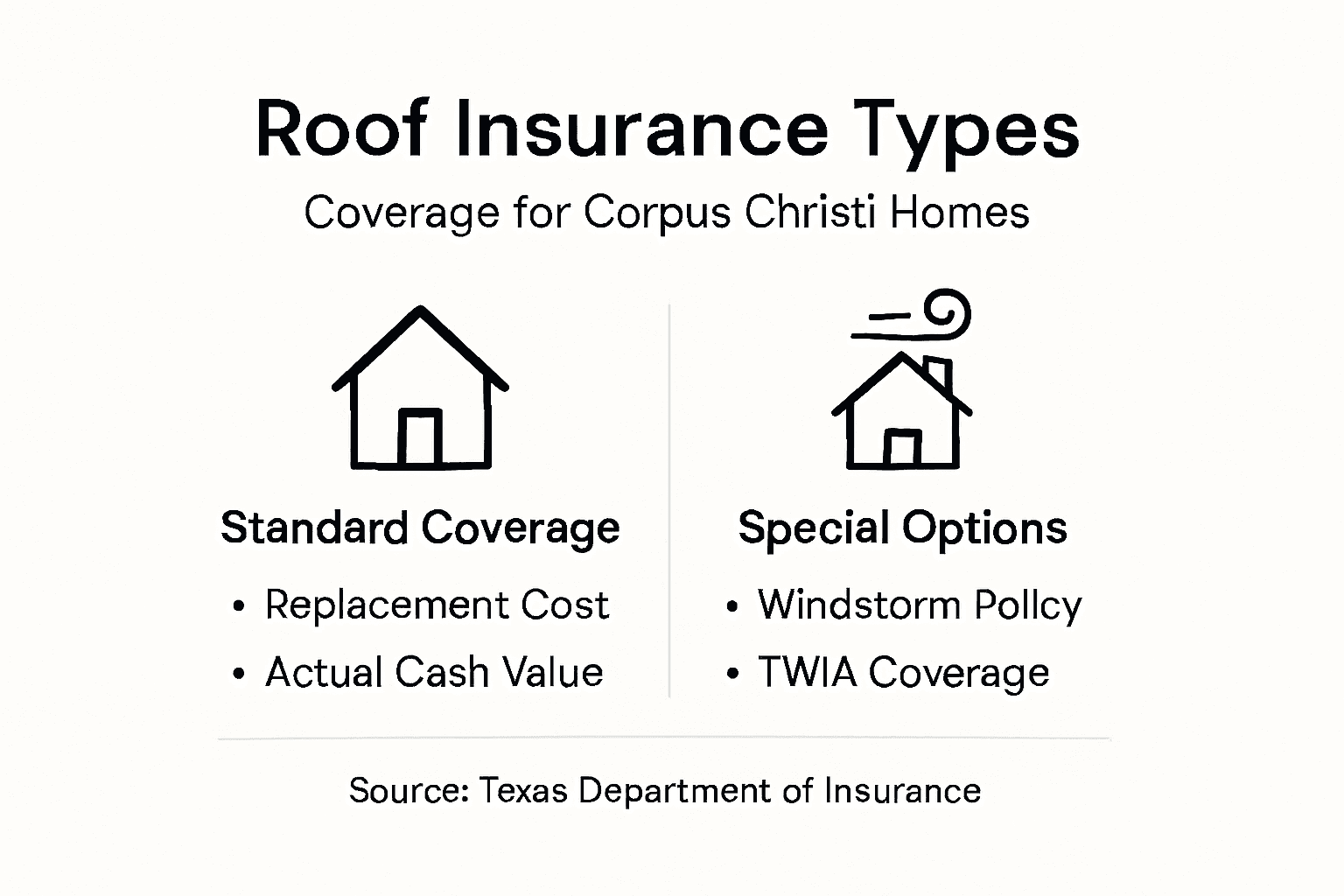

Types Of Roofing Insurance Coverage In Texas

In Texas, homeowners have multiple roofing insurance coverage options designed to protect against the state’s challenging weather conditions. The primary types of coverage include replacement cost coverage and actual cash value coverage, each offering distinct financial protections for roof damage. Windstorm and hail insurance represents a critical additional layer of protection, especially for coastal regions like Corpus Christi where severe weather events are common.

Replacement cost coverage provides the most comprehensive protection, paying the full expense of roof repair or replacement without accounting for depreciation. This means if a hurricane or major storm damages your roof, the insurance will cover the complete cost of restoring it to its original condition. Actual cash value coverage, conversely, factors in the roof’s age and current condition, potentially reducing the total payout based on the roof’s depreciated value. Homeowners should carefully evaluate which option provides the most financial security for their specific situation.

Texas offers specialized insurance options through the Texas Windstorm Insurance Association (TWIA), which provides targeted coverage for wind and hail damage in coastal counties. These policies often include unique endorsements like indirect loss coverage and extension of coverage for wind-driven rain. The specific policy details can vary significantly, making it crucial for homeowners to thoroughly review their individual policy terms and understand exactly what is and is not covered.

Here’s a side-by-side comparison of Texas roofing insurance coverage types:

| Coverage Type | What It Pays For | Factors Affecting Payout | Best For |

|---|---|---|---|

| Replacement Cost | Full repair or replacement cost | Policy limits, deductibles | New or well-maintained roofs |

| Actual Cash Value | Depreciated value based on age | Roof age, current condition | Older roofs, cost savings |

| Windstorm/Hail Endorsement | Wind and hail damage repairs | Location, building code compliance | Coastal region homeowners |

Pro tip: Request a comprehensive roof inspection before renewing your insurance policy to ensure you have the most appropriate coverage for your home’s current condition and potential weather risks.

How Roof Insurance Claims Work

The roof insurance claims process can be complex, but understanding the key steps helps Corpus Christi homeowners navigate potential storm damage repairs effectively. When roof damage occurs, the initial step involves documenting the destruction thoroughly through photographs and detailed professional inspections. These independent assessments create an objective record that supports your insurance claim and prevents potential disputes with insurance adjusters.

After documenting the damage, homeowners must contact their insurance provider to initiate the claims process. An insurance adjuster will be dispatched to evaluate the roof’s condition and assess the extent of damage. This professional will determine whether the damage qualifies for coverage based on your specific policy terms. Homeowners should be prepared to provide comprehensive documentation, including repair estimates from licensed roofing contractors, photographs of the damage, and any relevant maintenance records that demonstrate the roof’s prior condition.

The claims settlement typically involves multiple stages of payment. Initial checks are often considered advance payments, with final settlements negotiated based on comprehensive damage assessments. Mortgage lenders usually need to endorse these insurance checks to protect their financial interests. Importantly, homeowners should maintain open communication with their insurance company, carefully track all correspondence, and understand that the total claim amount may be distributed across several payments covering structural repairs, potential temporary housing, and additional living expenses.

Pro tip: Keep a comprehensive digital file of all roof-related documents, including inspection reports, repair estimates, and insurance communications, to streamline the claims process and protect your interests.

Windstorm And Weather-Related Coverage Rules

Corpus Christi homeowners must navigate complex windstorm insurance regulations specific to coastal Texas regions. Windstorm coverage eligibility depends on several critical factors, including property location, building code compliance, and proximity to coastal zones. The Texas Windstorm Insurance Association (TWIA) establishes strict guidelines that determine whether a property qualifies for specialized wind damage protection.

Homeowners insurance policies in Texas typically include unique exclusions for weather-related damages. Standard policies often do not cover flood damage or comprehensive windstorm protection, requiring separate insurance policies. Coastal properties must meet specific certification requirements, including proof of windstorm building code compliance and maintaining structures that can withstand severe weather conditions. Importantly, insurers may require additional documentation, such as windstorm inspections and certifications, to approve coverage for properties in high-risk areas.

The claims process for weather-related damages involves multiple complex considerations. Insurance policies in coastal regions frequently have specific deadlines for filing claims after weather events, and coverage can vary significantly based on the type of damage and geographic location. Homeowners must carefully review their policy terms, understanding the precise definitions of wind damage, hurricane impacts, and hail destruction to ensure adequate protection. Some policies may offer different levels of coverage for various weather-related events, making it crucial to understand the nuanced details of your specific insurance contract.

Pro tip: Conduct an annual review of your windstorm insurance policy, verifying that your coverage matches current building codes and potential regional weather risks.

Common Exclusions And Claim Pitfalls

Understanding the intricate landscape of insurance exclusions is crucial for Corpus Christi homeowners seeking comprehensive roof protection. Homeowners insurance claims frequently involve complex limitations that can catch property owners off guard. Typical exclusions range from flood damage and earthquake impacts to gradual wear and tear, creating potential financial vulnerabilities that many homeowners unknowingly face.

Water damage represents one of the most nuanced areas of insurance coverage. Policies typically distinguish between flood-related damage (usually not covered) and other forms of water intrusion. Roof-related claims can be denied for reasons including poor maintenance, gradual deterioration, or failure to address minor damages promptly. Homeowners must carefully document maintenance records, immediately report potential issues, and understand the precise definitions of covered and excluded damage types to maximize their potential for successful claims.

The claim filing process itself presents numerous potential pitfalls that can compromise insurance recovery. Insurance policy conditions often include strict documentation requirements, specific filing deadlines, and precise evidence standards. Incomplete documentation, delayed reporting, or misunderstanding policy terms can result in claim denials or significantly reduced settlements. Corpus Christi homeowners should maintain detailed records, photograph damage comprehensively, and communicate with insurers promptly and precisely to navigate these complex requirements effectively.

Below is a summary of common roof insurance exclusions and pitfalls Corpus Christi homeowners should watch for:

| Exclusion Type | Typical Reason for Denial | Homeowner Action Needed |

|---|---|---|

| Flood Damage | Not included in standard policies | Purchase separate flood insurance |

| Poor Maintenance | Neglect or lack of upkeep | Maintain and document repairs |

| Gradual Deterioration | Wear and tear not sudden damage | Schedule regular inspections |

| Late Claim Filing | Missed policy deadlines | Report damage promptly |

Pro tip: Create a dedicated digital folder with high-resolution photographs, maintenance records, and timestamped documentation of any roof damage to strengthen your potential insurance claim.

Financial Impact And Choosing The Right Policy

Corpus Christi homeowners face a complex insurance landscape with significant financial implications for roof protection. Texas homeowners insurance premiums often exceed $4,000 annually, driven by frequent severe weather events and escalating construction costs. The high-risk coastal environment means insurance companies carefully assess property vulnerabilities, potentially limiting coverage options and increasing financial burden for property owners.

Selecting the right insurance policy requires a strategic approach that balances comprehensive coverage with affordable premiums. Replacement cost coverage provides more robust financial protection compared to actual cash value options, though at a higher initial cost. Homeowners can mitigate expenses by implementing risk reduction strategies such as installing impact-resistant roofing materials, maintaining comprehensive property documentation, and exploring potential discounts for proactive home maintenance.

Policy selection strategies involve carefully evaluating multiple factors beyond simple premium costs. Location risk, home construction quality, roof age, and specific coverage limits all play crucial roles in determining appropriate insurance protection. Corpus Christi residents should consider specialized windstorm endorsements, understand precise policy exclusions, and recognize that cheaper policies might ultimately provide less financial security during critical repair scenarios.

Pro tip: Request comprehensive insurance quotes from multiple providers, comparing not just premium costs but also specific coverage details, deductibles, and endorsement options to ensure optimal financial protection.

Protect Your Corpus Christi Home With Expert Roofing Services

Understanding your roofing insurance options is essential, but facing storm damage without trusted professionals can be overwhelming. Corpus Christi homeowners know the stress of severe weather and the challenge of navigating complex claims while ensuring their roofs are properly repaired or replaced. Whether you need a thorough roof inspection before renewing your policy or expert assistance after unexpected damage, reliable solutions matter.

Take control today by partnering with Buffalo Roofing & Exteriors. Our experienced team specializes in roofing services designed to complement your insurance coverage and protect your investment. From storm damage restoration and new roof installations to minor repairs and maintenance, we provide trusted workmanship and transparent communication. Visit our Roofing Archives to learn more about our services and discover how we help Corpus Christi homeowners safeguard their properties. Schedule your free estimate now at Buffalo Roofing & Exteriors and ensure your home withstands whatever the Texas coast brings.

Explore additional support for your home’s needs at our Repairs Archives. Don’t wait for the next storm to act—secure your home with the experts who understand both roofing and insurance requirements.

Frequently Asked Questions

What is roofing insurance?

Roofing insurance is a specialized type of homeowner protection that covers the roof of a home against unexpected damage from events such as hurricanes, hailstorms, and other severe weather conditions.

What types of roofing insurance coverage are available?

In Texas, homeowners can choose between replacement cost coverage, which pays the full expense for roof repair or replacement without depreciation, and actual cash value coverage, which accounts for the roof’s age and condition, potentially lowering the payout.

How do I file a roof insurance claim?

To file a claim, document the damage with photographs and obtain a professional inspection. Then, contact your insurance provider to initiate the process, and be prepared to provide detailed documentation, including repair estimates and maintenance records.

What are common exclusions in roofing insurance?

Common exclusions include flood damage, issues arising from poor maintenance, and gradual deterioration. Homeowners should understand their policy terms and ensure they maintain regular roof upkeep to avoid claim denials.