Every Corpus Christi homeowner knows how relentless Gulf Coast storms can leave a roof battered and insurance paperwork stacking up fast. When storms hit Texas, understanding the ins and outs of your roof damage claim is crucial for protecting your home and wallet. This guide empowers you with essential documentation steps, details about deductible rules, and clear explanations of state laws so you can confidently handle your insurance claim from start to finish.

Table of Contents

- Defining Insurance in Roof Damage Claims

- Types of Roof Insurance Policies in Texas

- Filing and Documenting a Roof Claim

- Legal Requirements for Roof Claims in Texas

- Understanding Deductibles and Coverage Limits

- Mistakes to Avoid When Filing Claims

Key Takeaways

| Point | Details |

|---|---|

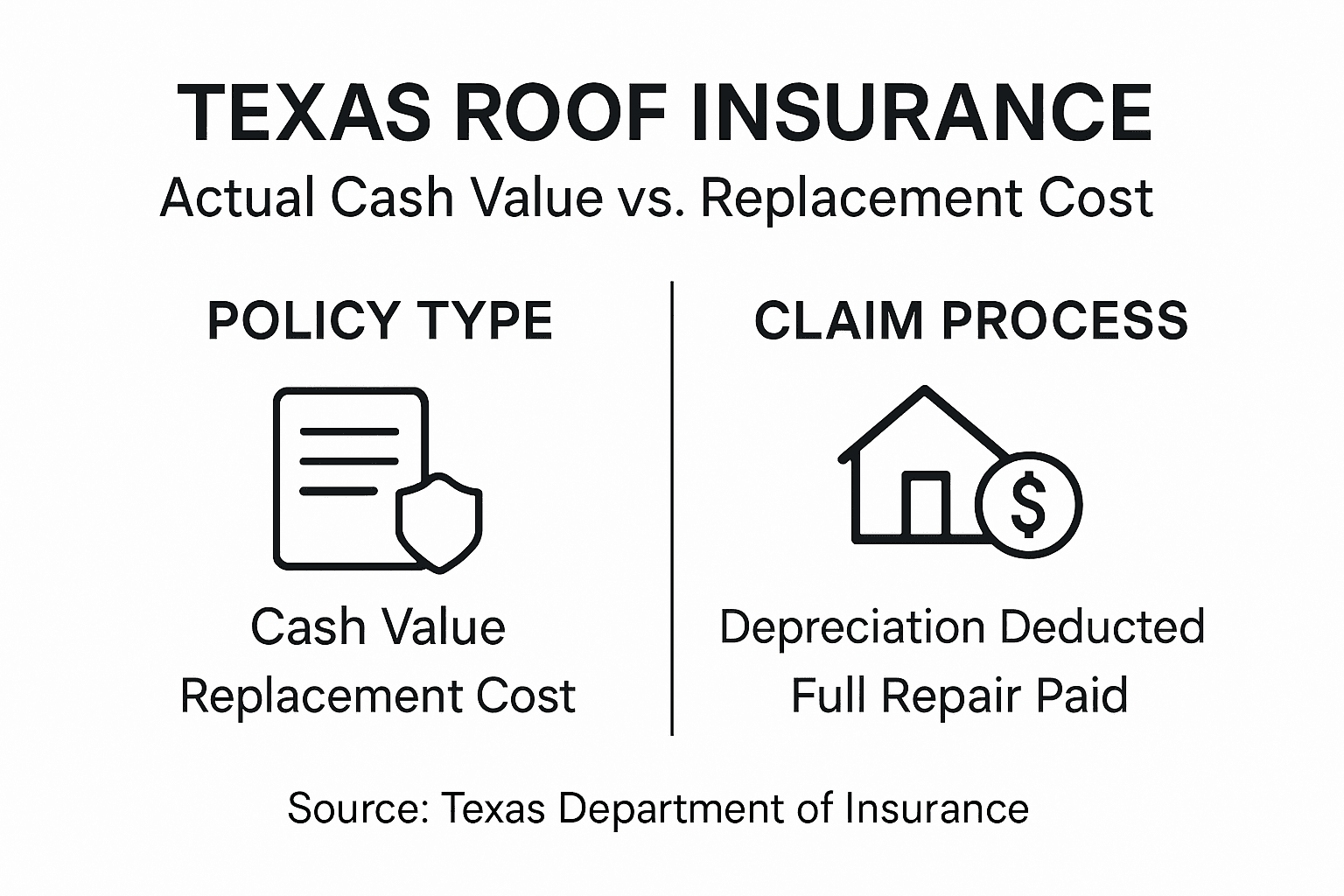

| Understanding Coverage | Homeowners must familiarize themselves with the distinctions between Actual Cash Value (ACV) and Replacement Cost Value (RCV) policies to choose the best protection against roof damage. |

| Documentation is Crucial | Thorough documentation of roof damage, including photographs and detailed descriptions, is essential for a successful insurance claim process. |

| Know Your Deductibles | Be aware of the types of deductibles in your policy, as this can significantly affect out-of-pocket expenses when filing a claim for roof damage. |

| Avoid Common Mistakes | Steer clear of documentation errors and miscommunication with insurance adjusters to prevent claim denials and ensure smoother processing. |

Defining Insurance in Roof Damage Claims

Understanding roof damage insurance is critical for homeowners in Texas, especially those living in storm-prone regions like Corpus Christi. Insurance claims for roof damage represent a complex process governed by specific state regulations and legal requirements. Homeowners must navigate these intricacies carefully to ensure proper compensation and protection.

In Texas, roof damage insurance claims involve several key components that homeowners should understand:

- Covered perils such as hail, windstorms, and hurricane damage

- Documentation requirements for filing successful claims

- Statute of limitations for reporting storm-related roof damage

- Deductible structures specific to different types of storm events

Texas Department of Insurance regulations clearly outline important legal boundaries in the claims process. Specifically, these regulations prohibit roofing contractors from simultaneously acting as public insurance adjusters, ensuring a clear separation between contracting and claims management services.

The claims process typically involves several critical steps. Homeowners must first document the damage thoroughly, including taking comprehensive photographs, obtaining professional roof inspections, and maintaining detailed records of all storm-related impacts. Insurance companies require substantial evidence to process claims effectively.

Navigating roof damage insurance requires understanding both your policy’s specific terms and broader Texas state insurance regulations. Different policies may offer varying levels of coverage, with some providing full replacement cost and others offering actual cash value based on the roof’s current age and condition.

Pro tip: Always review your insurance policy’s specific storm damage provisions before an emergency occurs and maintain a comprehensive photographic record of your roof’s condition.

Types of Roof Insurance Policies in Texas

Homeowners in Texas face unique challenges when it comes to roof insurance policies, particularly in storm-prone regions like Corpus Christi. Understanding the various types of coverage can mean the difference between financial protection and significant out-of-pocket expenses during severe weather events.

Texas roof insurance policies typically fall into several key categories:

- Actual Cash Value (ACV) Policies

- Reimburse homeowners based on the roof’s current market value

- Account for depreciation and age of the roofing materials

- Generally offer lower coverage amounts

- Replacement Cost Value (RCV) Policies

- Provide funds to replace the roof with similar quality materials

- Do not factor in depreciation

- Offer more comprehensive protection for homeowners

- Extended Coverage Policies

- Include additional protections beyond standard storm damage

- May cover wind, hail, and other specific weather-related risks

- Often include higher premium costs

Roofing insurance in Corpus Christi requires careful consideration of the unique weather challenges in coastal Texas. The type of policy you choose directly impacts your financial protection during storm events.

Most homeowners insurance policies in Texas include some level of roof damage protection, but the specifics can vary dramatically. Factors like the age of your roof, previous damage, and the specific terms of your policy can significantly influence your coverage. Some policies may have separate deductibles for wind and hail damage, which can be particularly important in storm-prone areas.

Insurance providers assess roof condition through detailed inspections, taking into account the roof’s age, material, and previous maintenance history. Older roofs or those with pre-existing damage may receive reduced coverage or require additional riders to ensure full protection.

Pro tip: Schedule an annual roof inspection and maintain detailed documentation of your roof’s condition to maximize your insurance coverage potential.

Here’s a quick comparison of actual cash value, replacement cost, and extended coverage roof insurance policies:

| Policy Type | Coverage Detail | Typical Out-of-Pocket Cost |

|---|---|---|

| Actual Cash Value (ACV) | Pays depreciated roof value | Usually lower upfront, higher later |

| Replacement Cost Value (RCV) | Pays full roof replacement, no depreciation | Higher premiums, lower final cost |

| Extended Coverage | Adds extra protections for specific risks | Highest premium, lowest risk |

Filing and Documenting a Roof Claim

Filing a roof insurance claim in Texas requires a strategic and methodical approach, especially for homeowners in storm-prone regions like Corpus Christi. Proper documentation can mean the difference between a successful claim and potential financial hardship.

The roof claim process involves several critical steps:

- Immediate Damage Assessment

- Conduct a thorough visual inspection of roof damage

- Take clear, timestamped photographs and videos

- Document all visible signs of storm-related destruction

- Evidence Collection

- Capture detailed images from multiple angles

- Include close-up and wide-angle shots

- Preserve evidence of water intrusion, missing shingles, and structural damage

- Insurance Claim Documentation

- Compile a comprehensive damage report

- Collect repair estimates from licensed contractors

- Maintain a chronological record of all storm-related damage

Texas roof insurance claims process requires meticulous attention to detail and prompt action. Homeowners should contact their insurance provider immediately after discovering roof damage, typically within 30-60 days of the storm event.

When filing a claim, insurance companies will require extensive documentation. This includes detailed photographs, contractor estimates, and a comprehensive description of the damage. Professional roof inspections can provide critical third-party verification of storm-related destruction, strengthening your claim’s credibility.

Texas homeowners should be aware of specific state regulations governing insurance claims. Some policies have unique provisions for wind and hail damage, and the claim process can vary depending on the specific terms of your insurance coverage. Understanding these nuanced requirements can significantly impact the success of your claim.

Pro tip: Create a digital and physical backup of all claim-related documentation, including photographs, estimates, and correspondence with your insurance provider.

Legal Requirements for Roof Claims in Texas

Texas homeowners navigating roof insurance claims must understand the complex legal landscape that governs property damage restoration. State regulations provide critical protections and guidelines designed to ensure fair treatment and transparent processes for property owners experiencing storm-related damage.

Key legal requirements for roof claims in Texas include:

- Contractor Restrictions

- Roofing contractors cannot act as public insurance adjusters

- Prohibited from negotiating insurance claims directly

- Must maintain clear separation between contracting and claims management

- Policyholder Protections

- Mandatory disclosure of insurance policy terms

- Timely claims processing requirements

- Protection against unfair claim denial practices

- Documentation Mandates

- Comprehensive damage documentation

- Detailed repair estimates

- Transparent communication with insurance providers

Texas property damage laws establish strict guidelines to protect homeowners during the insurance claims process. These regulations ensure that insurance companies cannot arbitrarily deny legitimate claims or engage in unethical practices.

The Texas Department of Insurance enforces specific regulations regarding roof damage claims. Homeowners must understand their rights and obligations, including the requirement to pay insurance deductibles and provide accurate documentation of storm-related damage. Some policies have unique provisions for wind and hail damage that can significantly impact claim outcomes.

Legal protections extend to preventing predatory practices by contractors and insurance providers. State law mandates clear communication, fair assessment of damages, and reasonable timelines for claim resolution. Homeowners should be aware of their rights to challenge claim decisions and seek independent assessments when necessary.

Pro tip: Consult with a legal professional specializing in insurance claims to understand the nuanced legal requirements specific to your roof damage situation.

Understanding Deductibles and Coverage Limits

Homeowners in storm-prone regions of Texas must navigate the complex world of insurance deductibles with precision and understanding. The financial implications of roof damage claims can be significant, making it crucial to comprehend how deductibles and coverage limits directly impact potential reimbursements.

Key components of insurance deductibles and coverage include:

- Deductible Types

- Percentage-based deductibles

- Fixed dollar amount deductibles

- Separate wind and hail deductibles

- Hurricane and named storm deductibles

- Coverage Limit Factors

- Roof age and condition

- Material type

- Previous damage history

- Replacement cost versus actual cash value

- Out-of-Pocket Expenses

- Initial deductible payment

- Potential depreciation costs

- Additional repair expenses

- Potential increased insurance premiums

Roof insurance claims in Texas require careful understanding of how deductibles function. Importantly, Texas law prohibits contractors from waiving deductibles, ensuring transparency and preventing potential insurance fraud.

Depreciation plays a critical role in determining actual claim payouts. Homeowners with actual cash value policies will see their reimbursement reduced based on the roof’s age and condition. Replacement cost value policies offer more comprehensive coverage, typically providing funds to replace the roof with similar quality materials.

Understanding your specific policy’s nuances is essential. Some policies have separate deductibles for wind and hail damage, which can significantly impact out-of-pocket expenses. Homeowners should carefully review their insurance documents and consult with their insurance provider to fully comprehend their financial responsibilities.

Pro tip: Maintain a detailed record of your roof’s maintenance history and take annual photographs to substantiate its condition for potential future insurance claims.

The table below highlights common deductible types and their financial impact on Texas homeowners:

| Deductible Type | How It Works | Impact During Claims |

|---|---|---|

| Percentage-Based | % of home insured value per claim | High cost for expensive homes |

| Fixed Dollar Amount | Set currency amount per claim | Predictable, easier to budget |

| Separate Wind/Hail | Distinct, higher for storm events | Increased storm out-of-pocket |

| Hurricane Named Storm | Applies to hurricane events only | Maximum exposure in disasters |

Mistakes to Avoid When Filing Claims

Navigation of roof insurance claims in Texas requires strategic precision and careful attention to detail. Claim filing mistakes can potentially derail your entire insurance settlement process, leaving homeowners financially vulnerable and frustrated with unexpected complications.

Common critical mistakes homeowners should avoid include:

- Documentation Errors

- Failing to photograph damage immediately

- Incomplete written damage descriptions

- Missing timestamped evidence

- Neglecting professional inspection reports

- Communication Missteps

- Admitting fault or speculating about damage causes

- Providing inconsistent information to adjusters

- Delaying initial claim notification

- Discussing case details without legal consultation

- Contractor Red Flags

- Working with unlicensed contractors

- Accepting offers to waive insurance deductibles

- Allowing unauthorized repairs before inspection

- Signing incomplete or vague repair contracts

Texas roof claims process demands meticulous documentation and strategic communication. Homeowners must understand that seemingly minor communication errors can significantly compromise their insurance settlement potential.

Insurance adjusters carefully evaluate every detail of a claim, making transparency and comprehensive documentation paramount. Exaggerating damage can be as detrimental as downplaying it, potentially triggering fraud investigations and claim denials. Homeowners should focus on providing clear, factual, and well-documented evidence of storm-related roof damage.

The legal landscape surrounding insurance claims is complex, with specific regulations governing how and when claims can be filed. Delays in reporting, incomplete documentation, and working with unscrupulous contractors can result in reduced settlements or complete claim rejections. Proactive, detailed, and strategic approach is crucial for successful roof damage claims.

Pro tip: Maintain a dedicated folder with all claim-related documents, including photographs, estimates, correspondence, and inspection reports, to streamline the claims process.

Protect Your Home with Trusted Roofing Solutions in Texas

Dealing with the complexities of roof damage insurance claims after a Texas storm can be overwhelming. From understanding deductibles to providing detailed documentation, the process demands precision and expertise. At Buffalo Roofing & Exteriors, we recognize the challenges homeowners face in storm-prone areas like Corpus Christi and are here to help you navigate repairs and restoration while maximizing your insurance benefits.

Explore our expert Roofing Archives for trusted guidance and quality craftsmanship. Don’t let storm damage disrupt your life or drain your finances. Visit Buffalo Roofing & Exteriors today to get a free estimate and start the path to a secure, weather-resistant roof. Act now for reliable repairs and peace of mind when you need it most.

Frequently Asked Questions

What types of roof damage are typically covered by insurance?

Roof damage from covered perils such as hail, windstorms, and hurricanes is usually included in insurance policies. Homeowners should review their specific policies to understand coverage details.

How do I document roof damage for an insurance claim?

To document roof damage effectively, take comprehensive photographs, gather professional inspection reports, and maintain a detailed record of all visible signs of storm-related damage.

What are the differences between Actual Cash Value and Replacement Cost Value policies?

Actual Cash Value policies reimburse homeowners based on the current market value after depreciation, while Replacement Cost Value policies reimburse for the total cost to replace the roof without factoring in depreciation.

What legal requirements must homeowners be aware of when filing a roof claim?

Homeowners should understand the restrictions on contractors acting as public adjusters, mandatory documentation requirements, and consumer protections against unfair claim denial as outlined by state regulations.