TL;DR:

- A fortified roof certification can significantly lower insurance premiums and bolster a home’s storm resilience in Texas.

- Strategic financing options like HELOCs, loans, and grants help homeowners fund upgrades that reduce long-term costs and risks.

- Proactive resilience investments backed by proper documentation and certifications improve insurance outcomes and overall home safety.

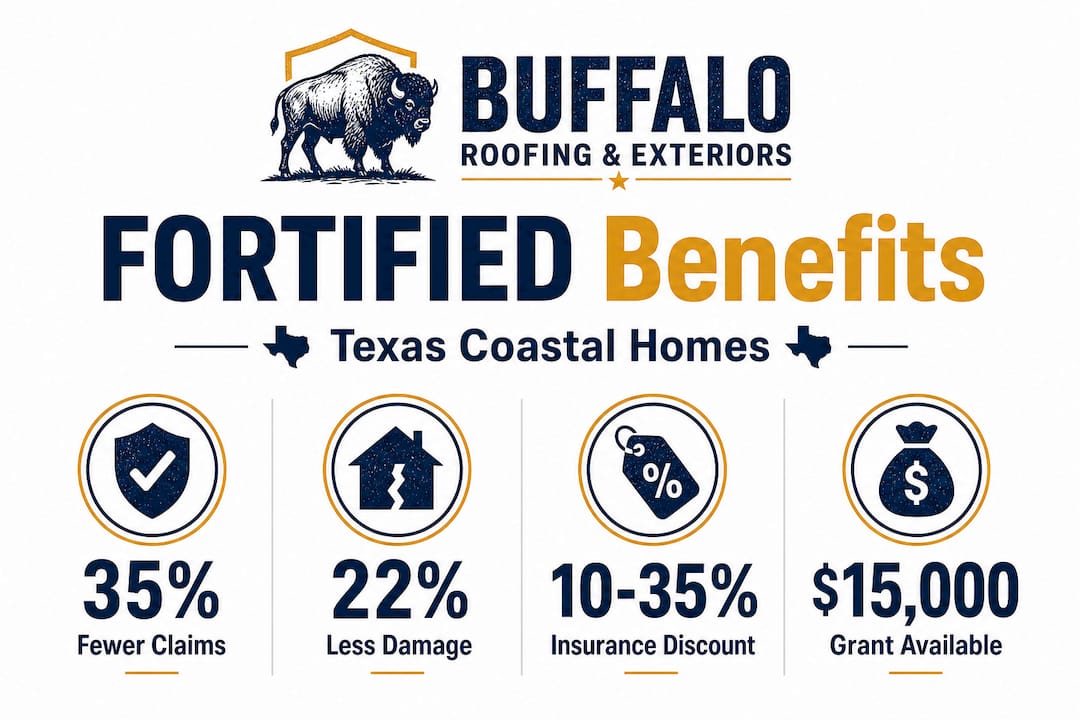

A FORTIFIED roof certification can save Texas coastal homeowners between $400 and $1,200 every year in insurance premiums alone, yet most people only think about financing when they need to cover a repair bill. That mindset leaves serious money on the table. Along the Gulf Coast, where a single hurricane season can batter siding, strip shingles, and push insurance rates even higher, smart financing isn’t just a payment plan. It’s a strategic tool that can reshape your home’s risk profile, reduce your long-term costs, and protect your investment for years after the contractor leaves.

Table of Contents

- Why financing matters for Texas coastal renovations

- Understanding the main financing options

- Maximizing value: Combining resilience and financing

- Common mistakes and myths in renovation financing

- Our take: Why renovation financing is your smartest storm defense

- Take the next step with your Texas renovation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Financing amplifies ROI | When used wisely, financing allows homeowners to unlock both immediate upgrades and long-term insurance and property value benefits. |

| Know your loan options | HELOCs, PACE, FHA 203k, and HomeStyle have very different terms and impact eligibility, risk, and payback. |

| Combine upgrades with resilience | Bundling storm-resistant features during renovation maximizes return through savings, especially in coastal Texas. |

| Avoid common mistakes | Missing Texas-specific limits, grants, or certification requirements can cost homeowners thousands. |

| Plan for more than repairs | The best renovation strategies turn necessary fixes into opportunities for improved storm defense and lower ongoing costs. |

Why financing matters for Texas coastal renovations

Texas coastal homeowners live with a reality that most of the country doesn’t fully appreciate. Storms roll in fast, damage accumulates season after season, and the cost of staying ahead of that damage keeps climbing. A roof that was fine five years ago may no longer meet updated wind resistance standards. Siding that looked solid before a tropical storm can hide moisture damage that compounds quietly until it becomes a very expensive problem.

Understanding why exterior renovations matter for coastal Texas homes goes beyond curb appeal. The real story is about resilience, insurance performance, and long-term financial health. Coastal homeowners who upgrade proactively instead of reactively almost always spend less over a ten-year window than those who patch and wait.

Here’s what makes financing so critical for Texans specifically:

- Storm frequency means repair costs aren’t a one-time event, they’re a recurring expense

- Insurance carriers are raising rates and tightening eligibility requirements along the Gulf Coast

- Resilience upgrades like FORTIFIED certification are not cheap upfront but generate measurable, documented savings

- Many homeowners simply don’t have $15,000 to $30,000 in cash sitting available for a full roof replacement or exterior overhaul

“Coastal Texas homeowners who pursue FORTIFIED certification aren’t just getting a better roof. They’re changing how insurers see their property, which directly affects what they pay every single year.”

The numbers back this up. FORTIFIED certification yields 10 to 35% insurance discounts in Texas, reduces claims by 35%, and lowers storm damage by 22%. Grants of up to $15,000 are also available through FHLB Dallas for low-income homeowners pursuing these upgrades. When you frame financing through that lens, borrowing money to make a resilience upgrade isn’t a liability. It’s a calculated investment with a documented payback period.

Understanding the main financing options

With the stakes established, the next step is knowing exactly what tools are available and how each one works in Texas’s specific legal environment. Not all loans are created equal, and Texas has some of the most consumer-protective home equity rules in the country, which matters a lot when you’re planning a major renovation.

The main financing options Texas coastal homeowners should know about include:

- HELOCs (Home Equity Lines of Credit): Flexible revolving credit secured by your home’s equity. Texas limits combined mortgage and HELOC borrowing to 80% of your home’s value, with rates currently in the 8 to 9% range. There’s a mandatory 12-day waiting period after application and a 3-day cancellation window after closing.

- Home equity loans: A lump-sum loan at a fixed rate, also subject to the 80% combined loan-to-value (LTV) rule in Texas. Good for defined project scopes where you know the total cost upfront.

- PACE loans (Property Assessed Clean Energy): Repaid through your property tax bill rather than a separate mortgage payment. Ideal for energy efficiency and storm resilience upgrades. These tend to carry fixed long-term rates and stay with the property if you sell.

- FHA 203(k) loans: Government-backed renovation loans that bundle your mortgage and renovation costs into one. Lower credit requirements than conventional loans, but strict standards on what qualifies and no luxury improvements allowed.

- Fannie Mae HomeStyle loans: A conventional option that offers more flexibility in what projects qualify, but requires higher credit scores and a larger financial commitment upfront.

For a direct comparison, here’s how the major options stack up:

| Loan Type | Best For | Credit Requirement | Key Limitation |

|---|---|---|---|

| HELOC | Flexible, multi-phase projects | Moderate | 80% LTV cap, variable rate |

| Home equity loan | Single defined project | Moderate | 80% LTV cap, Texas wait period |

| PACE | Resilience/energy upgrades | Flexible | Stays with property on sale |

| FHA 203(k) | Lower credit homeowners | Lower | Strict project standards |

| HomeStyle conventional | High-value renovations | Higher | Larger down payment needed |

Pro Tip: Before applying for any Texas home equity product, count the days carefully. The 12-day wait and 3-day cancellation rule means your project timeline needs to build in at least two weeks before funds can close. Plan ahead so delays don’t stall your contractor.

You can review our full renovation financing guide for more details on how these programs apply to specific project types. For homeowners curious about additional funding sources outside traditional home equity, additional financing options may also be worth reviewing.

The key difference between government-backed and conventional options in Texas comes down to flexibility versus accessibility. FHA 203(k) opens the door for homeowners with lower credit scores and smaller down payments, but the approval process is stricter and the list of qualifying projects is more rigid. Conventional loans through the HomeStyle program allow more creative renovation scope but demand more financial strength at the start.

Maximizing value: Combining resilience and financing

Knowing your loan options is one thing. Knowing how to use them strategically to maximize the return on every dollar you borrow is where most homeowners fall short. The real opportunity in coastal Texas isn’t just replacing a worn roof. It’s using a planned replacement as the entry point for upgrades that permanently improve how your home performs in a storm.

Storm-resistant roofing trends along the Texas coast consistently point in the same direction: integrating resilience during a scheduled replacement costs far less than adding it later. A FORTIFIED roof typically runs 10 to 25% more than a standard replacement, but that incremental cost is often covered within one to three years through insurance savings. After that, you’re simply banking the discount every year.

Here’s how to structure your approach for maximum impact:

- Start with an inspection tied to your insurance review. Before you borrow a dollar, understand exactly what your insurer requires for premium reductions and what your roof’s current condition means for your coverage. Regular roof inspections and insurance savings are more connected than most homeowners realize.

- Choose your loan type based on project scope. If you’re doing a full roof replacement and siding upgrade together, a home equity loan with a fixed rate gives you budget certainty. If you’re phasing the work over two or three years, a HELOC’s revolving structure lets you draw as you go.

- Stack certifications to maximize insurance leverage. FORTIFIED certification is the big one, but adding impact-resistant windows or reinforced garage doors can layer additional premium reductions on top of the roofing discount.

| Upgrade | Estimated Cost Premium | Annual Insurance Savings | Payback Period |

|---|---|---|---|

| FORTIFIED roof certification | +10 to 25% vs. standard | $400 to $1,200 | 1 to 3 years |

| Impact-resistant siding | +8 to 15% vs. standard | $150 to $400 | 2 to 4 years |

| Storm-rated windows | +12 to 20% vs. standard | $200 to $500 | 2 to 4 years |

The HELOC vs. PACE comparison is worth thinking through carefully. A PACE loan locks in a fixed rate over a longer term, which works well when you’re funding a single large resilience project and want predictable payments. A HELOC gives you a revolving credit line you can draw from multiple times, which suits phased projects but exposes you to rate changes over time if rates rise.

Pro Tip: When you finance a FORTIFIED upgrade, treat the first year’s insurance savings as a partial loan payment. Redirect that $400 to $1,200 directly back toward your principal balance to shorten the loan term and cut overall interest costs.

Common mistakes and myths in renovation financing

Even homeowners who do their research often stumble on a handful of predictable mistakes. These aren’t small errors. Some of them can mean thousands of dollars in missed savings or unexpected costs that blow up a renovation budget.

The most common mistakes and myths worth knowing:

- Treating renovation loans like a cash-out refinance. They’re fundamentally different products. A cash-out refinance replaces your existing mortgage and resets your rate. Renovation loans sit alongside it. Mixing them up can lead to unrealistic expectations about approval amounts.

- Assuming insurance savings are automatic. Simply installing a new roof doesn’t trigger a premium discount. Specific certifications, particularly FORTIFIED designation, must be formally documented and submitted to your insurer. Without that paperwork, you leave money behind.

- Ignoring Texas’s waiting periods. The 12-day application wait on Texas HELOCs catches people off guard when they’re eager to get started. Rushing the timeline doesn’t remove the legal requirement. Build it into your project plan from day one.

- Overlooking grant eligibility. Many qualifying homeowners never apply for FHLB Dallas grants simply because they didn’t know the program existed. If your household income qualifies, that’s up to $15,000 in funding you don’t have to pay back.

- Underestimating the LTV ceiling. Texas’s 80% combined LTV rule is firm. If your home has appreciated significantly, you may have more equity available than you think. If you’ve refinanced recently, you may have less. Know your actual numbers before you apply.

Understanding how insurance claims and roof replacement intersect can help you avoid the documentation gaps that delay or reduce claim payouts. Keep records of every upgrade, every certification, and every inspection. Those documents are your financial backstop when a storm rolls through.

Pro Tip: Create a dedicated home improvement folder, either physical or digital, that holds every permit, certification, warranty, and contractor receipt. When you file a claim or shop for better insurance rates, that folder is worth its weight in gold.

Our take: Why renovation financing is your smartest storm defense

Here’s the uncomfortable truth most financing articles won’t tell you directly. The homeowners who get hurt most after a major storm aren’t always the ones with the worst roofs. They’re often the ones who had decent roofs but no documentation, no certifications, and no relationship with their insurer built around demonstrable resilience.

Financing is the mechanism that makes proactive resilience upgrades possible for most families. But what really transforms the outcome is using that financing intentionally, not just to replace what broke but to make your home a fundamentally different risk profile in the eyes of your insurance carrier.

We’ve seen it play out repeatedly. A homeowner finances a standard roof replacement after a storm, pays it off, and then gets hit with a rate increase because they didn’t meet the updated wind mitigation requirements their insurer had quietly introduced. Another homeowner spends a little more, gets FORTIFIED certified, and sees their premium drop by $900 a year. Same neighborhood, same storm exposure, completely different financial outcomes.

The insurance claims process consistently rewards homeowners who can prove their home’s resilience on paper. And impact-resistant roofing that meets certification standards isn’t just about surviving a storm. It’s about what happens at renewal time when your insurer decides whether to keep your policy and at what rate.

The IBHS data is clear: FORTIFIED certification cuts claims by 35% and reduces storm damage by 22%. That’s not marketing language. That’s actuarial reality, which is exactly why insurers respond to it with meaningful discounts. When you finance a resilience upgrade strategically, you’re not just spending money on your home. You’re changing the math on what you’ll pay for years to come.

The best financing strategy isn’t the one with the lowest rate. It’s the one that connects your borrowing directly to a resilience outcome that pays you back through lower premiums, fewer claims, and a stronger home when the next storm arrives.

Take the next step with your Texas renovation

Knowing the right strategy is only useful when you act on it. If you’re weighing exterior upgrades, a new roof, or resilience improvements for your coastal Texas home, the next step is connecting with people who understand both the construction side and the financial side of making those investments count.

Explore real examples of how coastal renovation value translates to long-term savings for Texas homeowners. Whether you’re starting with a storm damage assessment or planning a full exterior upgrade from the ground up, Buffalo Roofing & Exteriors brings the expertise to help you build a plan that works. From weather-resistant roofing solutions to customized financing guidance, we’re here to help Corpus Christi, San Antonio, and Victoria area homeowners make the most of every dollar they invest in their home.

Frequently asked questions

How much can Texas homeowners borrow with a HELOC for renovations?

Texas law limits your combined mortgage and HELOC balance to 80% of your home’s appraised value, so your available borrowing depends directly on how much equity you’ve built above that threshold.

What makes PACE loans different from a standard home equity loan?

PACE loans are repaid through your property tax bill rather than a separate mortgage payment, and they focus on resilience or energy upgrades with fixed long-term rates, while HELOCs add revolving debt with more flexibility but variable rates.

Does installing a FORTIFIED roof affect insurance costs?

Yes, FORTIFIED certification yields 10 to 35% insurance discounts in Texas and also reduces claims by 35% and documented storm damage by 22%, making it one of the highest-ROI upgrades available to coastal homeowners.

Are there grants for low-income Texans upgrading roofs?

Yes, FHLB Dallas offers grants up to $15,000 for qualifying low-income Texas homeowners who are pursuing FORTIFIED roof certifications, so it’s worth checking eligibility before assuming financing is the only path.

What is the waiting period for Texas home equity loans?

Texas law requires a mandatory 12-day wait after you submit your application before closing can proceed, plus a 3-day cancellation window after you sign, so factor at least two weeks into your project timeline before funds become available.