TL;DR:

- Weatherproof exterior upgrades can reduce storm damage and insurance costs for Texas homeowners.

- Investing in impact-resistant roofing and sealed exteriors offers significant financial and safety benefits.

- Proactive upgrades improve home resilience, reduce repair costs, and increase property value long-term.

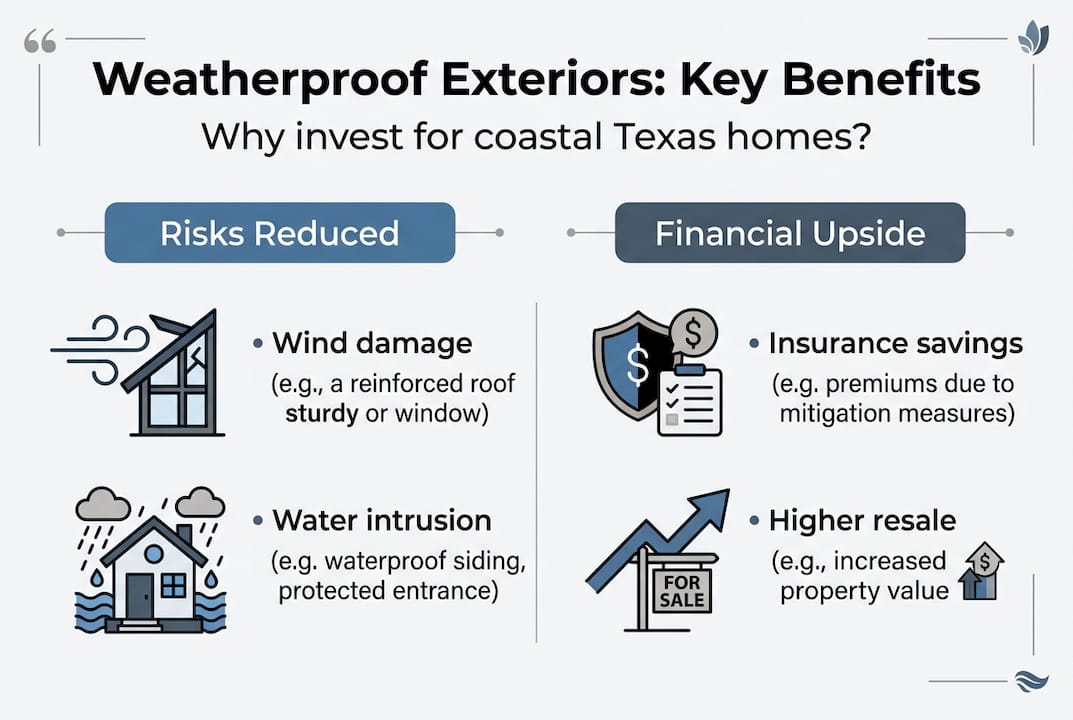

Upgrading your home’s exterior not only protects against powerful Gulf storms, but can also save you hundreds on insurance every year — yet most coastal Texas homeowners seriously underestimate these benefits. Homes with weather-resistant upgrades can qualify for insurance premium reductions of up to 35%, saving $400 to $1,200 annually. Along the Texas Gulf Coast, where hurricanes and tropical storms are a regular reality, your exterior is your first and most important line of defense. This guide walks you through what weatherproof exteriors actually are, how they protect your home, and why investing in them now makes more financial sense than waiting for the next storm to force your hand.

Table of Contents

- Understanding weatherproof exteriors: What they are and why they matter

- Financial benefits: ROI, insurance discounts, and property value

- Storm resilience: Evidence from Texas hurricane losses

- How to make smart exterior investments: Options, upgrades, and choosing the right contractor

- Our take: Why Texas homeowners should rethink exterior upgrades

- Next steps: Connect with trusted storm-ready exterior experts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Save on insurance | Weatherproof upgrades can reduce premiums by up to 35% and save $1,200 a year in coastal Texas. |

| Evidence-backed protection | Resilient exteriors prevent up to 73% of storm claims and dramatically lower hurricane-related losses. |

| Increase home value | Upgrading your home exterior boosts property value and makes your home more appealing to buyers. |

| ROI in just years | Most homeowners see payback from exterior investments within 2–10 years through avoided repairs. |

| Smart upgrade choices | Prioritize certified FORTIFIED roofs and weather-resistant materials for best long-term outcomes. |

Understanding weatherproof exteriors: What they are and why they matter

A weatherproof exterior is more than just a new coat of paint or a patched roof. It refers to a system of materials and construction methods designed to resist wind, rain, hail, and flooding — the exact conditions that batter coastal Texas homes every storm season. One of the most recognized standards in this space is the FORTIFIED designation, a building standard developed by the Insurance Institute for Business and Home Safety (IBHS). FORTIFIED, which stands for a specific set of construction criteria, certifies that a home’s roof, walls, and openings meet rigorous wind and impact resistance requirements.

To boost durability and savings, a truly weatherproof exterior typically includes four key components working together:

- Roofing: Impact-rated shingles or metal panels sealed against wind uplift

- Siding: Fiber cement or engineered wood that resists moisture and impact

- Windows and doors: Impact-resistant glass and reinforced frames rated for high wind pressure

- Seals and flashing: Waterproof barriers at every joint, edge, and penetration point

Coastal Texas homeowners face risks that inland properties simply don’t. Corpus Christi, Rockport, and surrounding communities sit in a zone where Category 3 and Category 4 hurricanes make landfall with alarming regularity. Salt air accelerates corrosion, sustained winds exceed 130 mph in major storms, and storm surge can push water into homes that aren’t properly sealed. Understanding how weatherproof exteriors work in this specific environment is critical to making the right upgrade decisions.

| Exterior component | Standard material | Weatherproof upgrade |

|---|---|---|

| Roof covering | 3-tab asphalt shingles | Impact-rated architectural shingles or metal |

| Siding | Vinyl or wood | Fiber cement or engineered composite |

| Windows | Single-pane aluminum | Impact-resistant double-pane with reinforced frames |

| Doors | Standard hollow-core | Steel or fiberglass rated for high wind pressure |

The payoff is real. Weather-resistant upgrades can reduce overall storm losses by up to 40%, which means less out-of-pocket repair cost and faster recovery after a storm.

Pro Tip: Prioritize upgrades on the components most exposed to weather. Your roof takes the most punishment in any storm, so starting there delivers the fastest return on both protection and insurance savings.

Financial benefits: ROI, insurance discounts, and property value

Now that we understand what weatherproof exteriors are, let’s examine the financial upside for coastal Texas homeowners.

The numbers are hard to ignore. Homeowners who achieve a FORTIFIED Roof certification can see wind coverage discounts of 20 to 35% on their insurance premiums, with payback periods ranging from 2 to 10 years depending on the scope of the upgrade and local insurance rates. In a market where wind and hail coverage has become increasingly expensive along the Texas coast, those savings add up fast.

Beyond insurance, weatherproof exteriors directly affect your home’s market value. Buyers in coastal markets actively look for homes that won’t require immediate storm repairs or carry high insurance costs. Here’s what you can expect from strategic exterior upgrades:

- Higher appraisal values due to certified storm-resistant construction

- Faster home sales because buyers feel confident in the home’s resilience

- Lower maintenance costs over time since quality materials resist wear longer

- Reduced repair bills after storms, which can run into tens of thousands for unprotected homes

The comparison between resilient and non-resilient exteriors tells a clear story:

| Factor | Non-resilient home | Resilient/FORTIFIED home |

|---|---|---|

| Annual insurance premium | $3,500 to $5,000+ | $2,300 to $3,500 |

| Post-storm repair cost (avg.) | $25,000 to $80,000 | $3,000 to $12,000 |

| Property value impact | Neutral to negative | Positive, 5 to 15% increase |

| Insurance claim frequency | High | Significantly lower |

Homes with upgrades that reduce storm damage by 60% or more are not just safer. They’re genuinely better financial assets. When you factor in avoided repairs, lower premiums, and higher resale value, the investment in exterior weatherproofing results often outperforms other common home improvements.

Storm resilience: Evidence from Texas hurricane losses

Financial benefits alone are compelling, but the true value of weatherproofing shows up during storms. Let’s dig into the data.

Hurricane Harvey in 2017 left a devastating mark on the Texas coast. 161,000 homes were damaged in the Houston area alone, with total losses running into billions of dollars. The contrast between homes with resilient features and those without was stark. Homes built or upgraded to higher standards experienced dramatically less structural damage, required fewer emergency repairs, and moved through the insurance claims process far more quickly.

Here’s what the evidence shows across multiple major storms:

- Hurricane Harvey (2017): Homes with impact-resistant roofing had significantly lower interior water damage compared to homes with standard shingles

- Hurricane Ike (2008): Galveston-area homes with reinforced windows and doors retained structural integrity at much higher rates

- Hurricane Laura (2020): FORTIFIED-certified homes in Louisiana showed minimal roof damage while neighboring homes lost entire roof sections

- Hurricane Sally (2020): IBHS data confirmed that FORTIFIED roofs outperformed standard construction in every tested wind speed category

“Resilient features reduce insurance claims by 73% compared to standard construction homes in comparable storm conditions.”

That figure changes the entire conversation. It’s not just about surviving a storm. It’s about how quickly you recover, how much you pay out of pocket, and whether your family can stay in their home while repairs happen.

| Storm event | Avg. damage: standard home | Avg. damage: resilient home |

|---|---|---|

| Category 1 to 2 hurricane | $8,000 to $20,000 | $1,500 to $4,000 |

| Category 3 hurricane | $30,000 to $60,000 | $5,000 to $15,000 |

| Tropical storm with hail | $5,000 to $12,000 | $500 to $2,500 |

Investing in damage reduction upgrades before a storm arrives is the difference between a minor inconvenience and a financial crisis. The data from upgrading home exteriors in coastal Texas consistently shows that proactive investment beats reactive repair every single time.

How to make smart exterior investments: Options, upgrades, and choosing the right contractor

Armed with storm-tested evidence and financial data, it’s time to turn insights into action by choosing the right exterior upgrades.

Not every upgrade delivers equal value. The key is prioritizing improvements that address your home’s biggest vulnerabilities first. Here’s a practical sequence to follow:

- Start with the roof. It’s the most exposed component and the one that drives the largest insurance discounts when upgraded to FORTIFIED standards

- Reinforce windows and doors. Impact-resistant openings prevent wind and water from entering and causing catastrophic interior damage

- Upgrade siding. Fiber cement siding resists moisture, impact, and salt air far better than vinyl or wood alternatives

- Seal all penetrations. Flashing, caulking, and waterproof membranes at every joint and edge prevent slow water intrusion that leads to mold and rot

- Consider financing options. Many contractors offer payment plans, and some utility programs and state initiatives help offset upgrade costs

Choosing the right contractor matters as much as choosing the right materials. Look for contractors with verifiable local experience, not just general credentials. Ask specifically about their familiarity with coastal Texas building codes, which are stricter than inland requirements for good reason. Verify that they can facilitate FORTIFIED certification if that’s your goal, since not every contractor is authorized to complete the required documentation.

It’s also worth noting that benefits vary by insurer, so ask your insurance agent upfront which upgrades will trigger a discount before you commit to a specific project scope. Some carriers reward full FORTIFIED certification, while others offer partial credits for individual improvements like impact windows or reinforced roofing.

When evaluating weather-resistant options for your home, compare material warranties, wind ratings, and local availability. The best storm-ready materials are those that meet or exceed Texas Windstorm Insurance Association (TWIA) requirements.

Pro Tip: Ask every contractor you interview whether they have experience with FORTIFIED certification and whether they’ve worked on homes in your specific zip code. Local storm history varies significantly, and a contractor who knows your neighborhood’s vulnerabilities will give you far better recommendations.

Our take: Why Texas homeowners should rethink exterior upgrades

Here’s the reality we see again and again working with coastal Texas homeowners: most people only invest in exterior upgrades after a major storm forces their hand. By then, they’re paying emergency rates, competing with thousands of other homeowners for contractor availability, and dealing with the emotional and financial stress of serious damage.

The conventional wisdom says “wait and see.” We think that’s a costly mistake. After more than 15 years working on coastal exteriors, we’ve watched proactive homeowners come through hurricanes with minimal damage and fast insurance settlements, while their neighbors face months of displacement and massive out-of-pocket costs.

Weatherproofing is not just a protection strategy. It’s a wealth-building strategy. The homes that hold their value best in coastal Texas markets are the ones with documented resilience upgrades. Buyers pay more for them, insurers reward them, and storms spare them. Understanding weatherproof exteriors protection as a long-term investment, not just a repair cost, is the mindset shift that separates smart homeowners from reactive ones.

Next steps: Connect with trusted storm-ready exterior experts

You now have the knowledge to make a confident, informed decision about protecting your coastal Texas home. The next move is connecting with professionals who can assess your specific situation and recommend the right upgrades for your budget and risk level.

At Buffalo Roofing & Exteriors, we specialize in helping Corpus Christi, San Antonio, and Victoria homeowners build durable, storm-ready exteriors. Whether you’re starting with a roof replacement or planning a full exterior overhaul, our team can guide you through every step. Explore our exterior renovation guide to understand your options, review our storm damage restoration resources, or browse weather-resistant roofing options built for the Gulf Coast. Contact us today for a free estimate.

Frequently asked questions

How much can I save on insurance by weatherproofing my home?

You can save 10 to 35% on wind coverage, which typically translates to $400 to $1,200 annually depending on your insurer and the scope of your upgrades.

Which exterior upgrades have the biggest impact against storms?

FORTIFIED roofs, impact-resistant windows and doors, and reinforced siding provide the highest storm resilience. FORTIFIED roofs specifically outperformed standard construction in hurricanes Sally, Ida, and Laura.

Do all insurance companies offer discounts for weatherproof exteriors?

Discounts vary by insurer; some carriers reward full FORTIFIED certification while others offer partial credits for individual improvements like impact windows or upgraded roofing.

How quickly do weatherproof investments pay off?

Most homeowners see a payback period of 2 to 10 years through a combination of avoided repair costs, lower insurance premiums, and increased property value.